Key Points

-

Nike has lost more than half its value in the past five years.

-

The stock is facing headwinds like U.S. tariffs and declining revenue in China.

-

Its CEO has a turnaround plan, but the athletic footwear market might be in decline.

-

Nike (NYSE: NKE) is an iconic brand that has launched world-famous products and eye-catching ad campaigns. But the apparel company, known for Air Jordans and other celebrity athlete endorsements, is struggling to gain liftoff in today’s consumer economy.

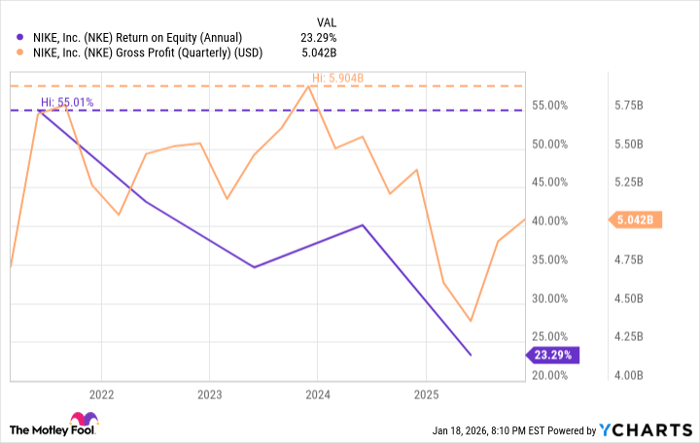

Nike stock is down 53% in the past five years. In the past four years, its return on equity has dropped from 43.1% in 2022, to 23.3% in 2025. The company’s quarterly gross profits have mostly gone in the wrong direction since 2023.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

NKE Return on Equity (Annual); data by YCharts.

What happened to the stock, and can it ever recover? Let’s look at the latest trends shaping the business’ performance, why this consumer discretionary stock has suffered, and whether investors should feel confident or cautious about Nike’s future.

Nike is being hit by tariffs

Just like many other apparel stocks, Nike is vulnerable to tariffs because it imports its shoes to the U.S. from a global supply chain. On its quarterly earnings call in September 2025, management said it expected tariffs to cost it $1.5 billion in fiscal year 2026, with a tariff-related reduction of 1.2% to its gross margin.

Image source: The Motley Fool.

Nike is facing tough competition in China

The company announced its latest earnings for the second quarter of fiscal 2026 on Dec. 18, 2025. Even though earnings per share beat analysts’ expectations, the stock price dropped 10% the day after the earnings call. That drawdown was driven by disappointing news from China, where the quarter’s total revenue from the Greater China market were down 17% compared to the previous year.

This is a sign that China is becoming an increasingly important market for Nike. If Chinese consumers stop buying its shoes, the company’s future growth could stall.

Consumers are more price-sensitive about shoes

The company wants to be a premium brand that can charge full price for its shoes. CEO Elliott Hill was hired in October 2024 to lead a turnaround. He is working to undo moves made by the previous leadership, which focused on helping expand its e-commerce by selling shoes directly to consumers online at a discount. Now, Hill is embracing a strategy of rebuilding Nike’s relationships with its wholesale channel partners and regaining shelf space at brick-and-mortar retailers.

But Nike and other shoe brands might face some challenges in raising prices. U.S. consumers seem to be getting choosier about how much they spend on shoes. The Footwear Distributors and Retailers of America (FDRA) released survey data in October 2025 showing that 48% of U.S. consumers were not planning to buy footwear during the 2025 holiday season, and 65% of likely shoe shoppers agreed that tariffs were a major reason why prices had gone up.

An FDRA survey of shoe executives this month shows that many tariff-related cost increases for shoes are still in the early stages. It found that 29.8% of shoe executives expect their average retail price to go up by 6% to 10%, while another 14.9% expect their average retail price to increase by more than 10%.

If shoe prices go up in a way that makes price-conscious customers close their wallets, Nike might struggle to regain its pricing power. And that could put downward pressure on margins.

Sports “casualization” could be ending

Athletic footwear brands built their businesses in part because of changing consumer behavior around wearing athletic shoes outside of the gym. They have become everyday casual wear at home and office for millions of people.

But if consumer styles and preferences change, this trend could fade away. If shoppers stop thinking it’s cool to wear sports shoes in casual settings, Nike’s business could suffer.

Recent research from Bank of America shows that this “casualization” trend in wearing athletic shoes might not have any more room to run. The bank’s analysts said that sneakers already represent about 50% of global footwear sales, and U.S. participation in sports is not growing. If the market for casual sports shoes is already saturated, this could be bad news for Nike and other athletic apparel brands.

People love sneakers, so it’s hard to believe that the global market for athletic shoes will severely decline anytime soon. But Nike can’t count on brand awareness alone to drive growth. It needs to innovate and create a new generation of must-have shoes that get people to wait in line at the mall. If not, the company is facing strong headwinds that could lead to a future of low growth and shrinking margins.

Should you buy stock in Nike right now?

Before you buy stock in Nike, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nike wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004… if you invested $1,000 at the time of our recommendation, you’d have $470,587!* Or when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $1,091,605!*

Now, it’s worth noting Stock Advisor’s total average return is 930% — a market-crushing outperformance compared to 192% for the S&P 500. Don’t miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of January 22, 2026.

Bank of America is an advertising partner of Motley Fool Money. Ben Gran has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Nike. The Motley Fool has a disclosure policy.